Tag Archive for: Women

https://prosperion.us/wp-content/uploads/2021/07/box-of-chocolates.jpg

430

1000

Danny Kellogg

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Danny Kellogg2021-07-14 14:57:512021-07-14 14:57:51Many Americans Face a Bitter-Sweet Early Retirement. What Should They Do?

https://prosperion.us/wp-content/uploads/2021/07/box-of-chocolates.jpg

430

1000

Danny Kellogg

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Danny Kellogg2021-07-14 14:57:512021-07-14 14:57:51Many Americans Face a Bitter-Sweet Early Retirement. What Should They Do? https://prosperion.us/wp-content/uploads/2021/04/pigg-bank.png

468

936

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-04-21 14:30:562021-04-21 14:31:155 Important Actions To Take During Financial Literacy Month

https://prosperion.us/wp-content/uploads/2021/04/pigg-bank.png

468

936

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-04-21 14:30:562021-04-21 14:31:155 Important Actions To Take During Financial Literacy Month https://prosperion.us/wp-content/uploads/2021/03/woman-doing-taxes.jpg

624

936

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-03-11 09:33:242021-03-11 09:33:24How Women Business Owners Can Save For Retirement And Reduce Taxes

https://prosperion.us/wp-content/uploads/2021/03/woman-doing-taxes.jpg

624

936

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-03-11 09:33:242021-03-11 09:33:24How Women Business Owners Can Save For Retirement And Reduce Taxes https://prosperion.us/wp-content/uploads/2021/02/forbes-top-advisors-steve-booren.png

1292

2658

LPL Financial

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

LPL Financial2021-02-23 11:27:472021-02-23 11:27:47PRESS RELEASE: Steve Booren Recognized in Forbes as a 2021 Best-in-State Wealth Advisor

https://prosperion.us/wp-content/uploads/2021/02/forbes-top-advisors-steve-booren.png

1292

2658

LPL Financial

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

LPL Financial2021-02-23 11:27:472021-02-23 11:27:47PRESS RELEASE: Steve Booren Recognized in Forbes as a 2021 Best-in-State Wealth Advisor https://prosperion.us/wp-content/uploads/2021/02/Picture1.jpg

312

624

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-02-22 11:30:332021-02-22 11:30:33What I Do & How I Help

https://prosperion.us/wp-content/uploads/2021/02/Picture1.jpg

312

624

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-02-22 11:30:332021-02-22 11:30:33What I Do & How I Help https://prosperion.us/wp-content/uploads/2021/01/2021-pathway.png

391

977

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-01-25 17:30:512021-01-25 17:30:51It’s A New Year! Is It Time To Reevaluate Your Financial Plan?

https://prosperion.us/wp-content/uploads/2021/01/2021-pathway.png

391

977

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2021-01-25 17:30:512021-01-25 17:30:51It’s A New Year! Is It Time To Reevaluate Your Financial Plan? https://prosperion.us/wp-content/uploads/2021/01/world-is-temporarily-closed.jpg

868

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2021-01-05 13:48:002021-01-05 13:48:00Improving Investor Behavior – Hindsight in 2020

https://prosperion.us/wp-content/uploads/2021/01/world-is-temporarily-closed.jpg

868

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2021-01-05 13:48:002021-01-05 13:48:00Improving Investor Behavior – Hindsight in 2020 https://prosperion.us/wp-content/uploads/2020/12/gold.jpg

657

1500

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2020-12-07 10:09:462020-12-07 10:09:46Why Do People Really Buy Gold And What Are The Alternatives?

https://prosperion.us/wp-content/uploads/2020/12/gold.jpg

657

1500

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2020-12-07 10:09:462020-12-07 10:09:46Why Do People Really Buy Gold And What Are The Alternatives? https://prosperion.us/wp-content/uploads/2020/10/Your-7-Point-Checklist-For-When-Life-Suddenly-Changes.jpg

512

1024

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2020-10-27 09:38:052020-10-27 09:38:05Your 7-Point Checklist For When Life Suddenly Changes

https://prosperion.us/wp-content/uploads/2020/10/Your-7-Point-Checklist-For-When-Life-Suddenly-Changes.jpg

512

1024

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2020-10-27 09:38:052020-10-27 09:38:05Your 7-Point Checklist For When Life Suddenly Changes https://prosperion.us/wp-content/uploads/2020/10/woman-with-glasses.png

468

936

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2020-10-01 13:54:112020-10-01 13:54:11Your Comprehensive Financial Planning Guide For Women

https://prosperion.us/wp-content/uploads/2020/10/woman-with-glasses.png

468

936

Nelisha Firestone

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Nelisha Firestone2020-10-01 13:54:112020-10-01 13:54:11Your Comprehensive Financial Planning Guide For Women https://prosperion.us/wp-content/uploads/2020/04/cares-act-highlights.jpg

500

1200

Administrator

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Administrator2020-04-03 10:11:442020-04-03 12:02:25Highlights of the CARES Act

https://prosperion.us/wp-content/uploads/2020/04/cares-act-highlights.jpg

500

1200

Administrator

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Administrator2020-04-03 10:11:442020-04-03 12:02:25Highlights of the CARES Act https://prosperion.us/wp-content/uploads/2020/03/cycle-of-market-emotions.jpg

434

1010

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

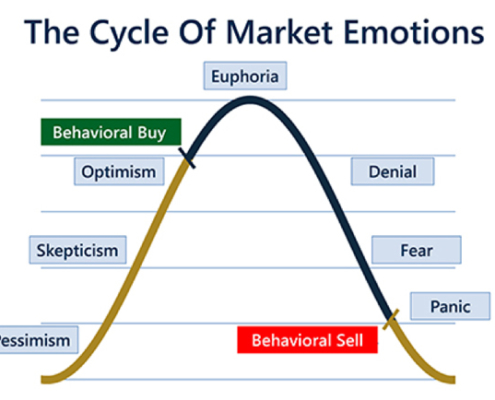

Steve Booren2020-03-20 11:55:122020-03-20 12:45:41Timeless Truths & The Cycle of Market Emotions

https://prosperion.us/wp-content/uploads/2020/03/cycle-of-market-emotions.jpg

434

1010

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2020-03-20 11:55:122020-03-20 12:45:41Timeless Truths & The Cycle of Market Emotions https://prosperion.us/wp-content/uploads/2020/03/panic.jpg

816

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2020-03-12 09:10:342020-03-12 09:10:34Improving Investor Behavior – Investing in Panic

https://prosperion.us/wp-content/uploads/2020/03/panic.jpg

816

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2020-03-12 09:10:342020-03-12 09:10:34Improving Investor Behavior – Investing in Panic https://prosperion.us/wp-content/uploads/2020/02/rollercoaster-e1582906425919.jpg

825

1496

Administrator

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Administrator2020-02-28 09:19:222020-02-28 09:20:02A Note to Clients on Virus Volatility

https://prosperion.us/wp-content/uploads/2020/02/rollercoaster-e1582906425919.jpg

825

1496

Administrator

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Administrator2020-02-28 09:19:222020-02-28 09:20:02A Note to Clients on Virus Volatility https://prosperion.us/wp-content/uploads/2020/01/steve-booren-forbes-top-advisor.png

1328

2732

LPL Financial

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

LPL Financial2020-01-31 08:45:262020-01-31 08:45:26PRESS RELEASE: Steve Booren Recognized in Forbes as a 2020 Top Wealth Advisor in Colorado

https://prosperion.us/wp-content/uploads/2020/01/steve-booren-forbes-top-advisor.png

1328

2732

LPL Financial

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

LPL Financial2020-01-31 08:45:262020-01-31 08:45:26PRESS RELEASE: Steve Booren Recognized in Forbes as a 2020 Top Wealth Advisor in Colorado