Timeless Truths & The Cycle of Market Emotions

Just 30 days ago, on Feb. 18th, markets were at all-time highs. Today, fear grips the market and recession is at the top of every financial pundits’ mind. Benjamin Graham, said to be one of the best investors of all time, and a mentor to Warren Buffett reminds us:

Control what you can control: yourself, your emotions and your response (or behavior) to those emotions.

Through many of the articles I’ve read this week, one stood out to me. Here’s an excerpt, written by the Collaborative Fund:

The majority of your lifetime investment returns will be determined by decisions that take place during a small minority of the time.

Most of those periods come when everything you thought you knew about investing is thrown out the window.

How you invested from 1990 to 1998 wasn’t all that important. The choices you made from 1999 to 2001 shaped the rest of your investing career.

What you did from September 2008 to March 2009 likely had more impact on your lifetime investment returns than what happened cumulatively from 2002 to 2007, or from 2009 to 2017.

The pilot’s famous answer when asked about his job — “Hours of boredom punctuated by brief moments of terror” — applies perfectly to investing. The brief moments of terror are the rise and fall of markets like this.

Ask yourself: Am I a speculator or an investor? What is the difference?

A speculator looks at price and direction. They buy something, hoping it will rise for some reason, then sell to someone else with similar hopes. In effect they “rent” stocks with one thing in mind: price appreciation, then sell and move on. We call this Growth for Income.

An investor is someone who invests in a company (rather than a stock). They don’t view this as investing in a market, rather investing in great companies that are available for purchase from the stock market. Rather than thinking about price or attempting to speculate what the price may do over a short period of time, investors look deeper into what a company does, who they sell their product or services to, improvement in those sales, and a myriad of other underlying indications of a healthy and profitable business. The mindset is one of an owner rather than a renter (or speculator). We call this Growth of Income.

Benjamin Graham would describe price fluctuation as temporary. Declining prices offer opportunities to buy valuable assets at lower prices. In time the price rises, and the company becomes more fully valued. From his book often referred to as “the bible for investors”, Intelligent Investor:

“The investor’s primary interest lies in acquiring and holding suitable securities at suitable prices,” Graham wrote. The speculator, on the other hand, cares mainly about “anticipating and profiting from market fluctuations.”

If you’re an investor, “price fluctuations have only one significant meaning,” according to Graham: “an opportunity to buy wisely when prices fall sharply and to sell wisely when they advance a great deal.”

“The investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into a basic disadvantage,” warned Graham. He “would be better off if his stocks had no market quotation at all, for he would then be spared the mental anguish caused him by other persons’ mistakes of judgment.”

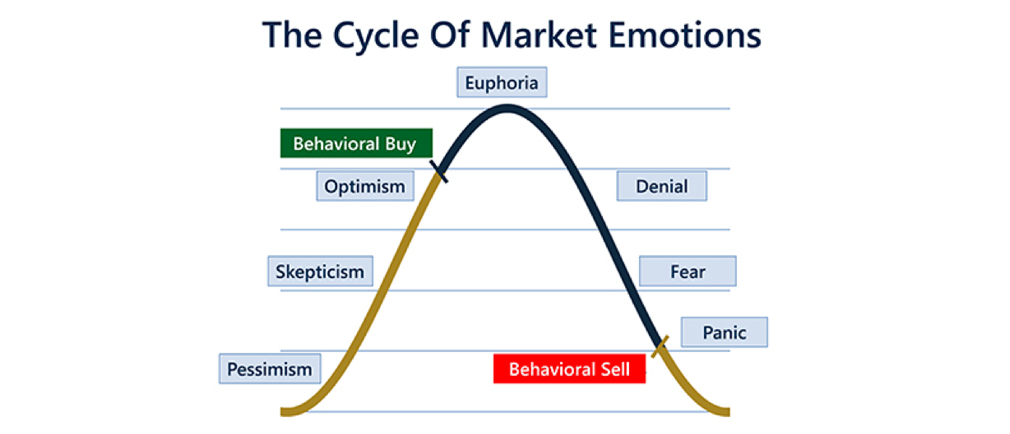

The primary reason many individuals fail as long-term investors, Graham said in 1972, is that “they pay too much attention to what the stock market is doing currently.”

Paying attention to today’s prices hitches investors to the emotions of greed and fear. The chart above exemplifies what those emotions feel like, and correlates investor behavior. It is emotion that drives many investors’ decisions, which in turn harm their investment results.

Consider a hypothetical company: Broadly diversified from consumer products to industrial utilities, this company is valued at $425. The company has $135 in it’s checking account. After doing business all year long, they generate $35/year in cash flow added each year to the checking account. Interestingly the company price per share has fallen some 20 percent due to the market declining 22 percent. That may seem odd, as over 25 percent of the company’s value is in cash, and cash should not decline like this. Stated another way, today you can buy $1 of the company for about $0.80. Looks interesting doesn’t it?

Add a billion to each of those numbers and the company you have is Berkshire Hathaway. Just three months ago Wall Street was lamenting that Warren Buffett must be asleep with $135B in cash. Imagine the smirk on his face today with that much “dry powder” to go out and invest in companies at what appear to be low prices. Or he could buy shares of his own company, spending $0.80 to get back $1. My hunch is he may do both.

Warren Buffett, a student of Graham, reminds us more than ever today: “The investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into a basic disadvantage.” -Benjamin Graham

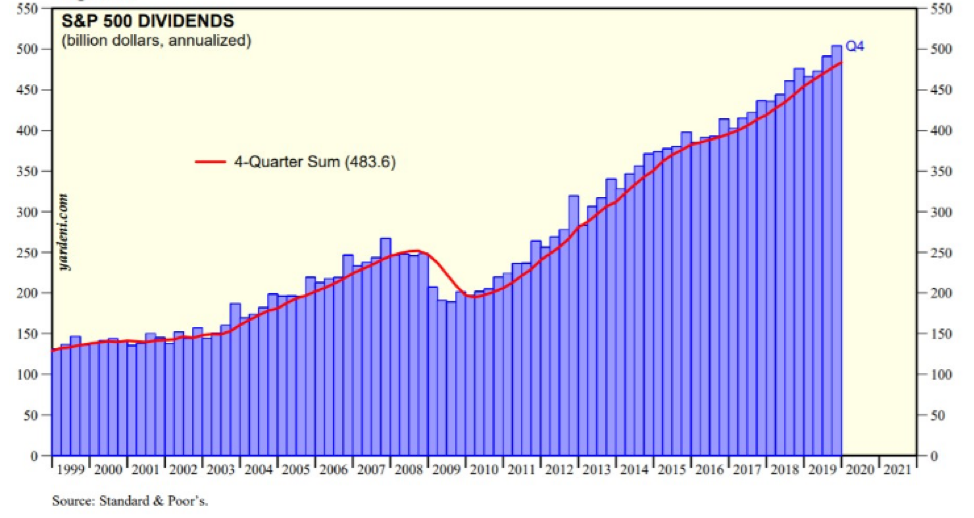

A picture of Dividends of the S&P 500 over the past twenty years.

It is important to understand our Investment Philosophy and Strategy

- The only reason people invest is for income – income today or income tomorrow

- Growing your income at a rate greater than the inflation rate protects the purchasing power of your money, enabling you to buy the same or more goods and services in the future.

Dividends are paid from revenues and profits of a company. They are not dependent nor have a correlation with the price per share of a company. People spend the income off the portfolio, not the value of their portfolio. Emotional responses of feeling “good” when prices are rising or high, and “bad” feelings when prices are falling or low is normal, but something to counter with logic.

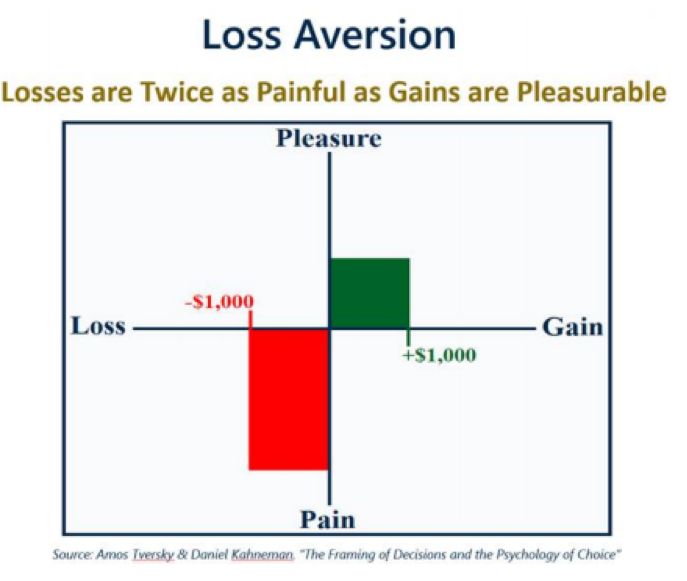

Loss Aversion

Remember, feeling bad when prices decline hurts twice as bad as the comparative good feelings when prices rise. (or stated to the chart below, losses feel twice as bad as gains feel pleasurable).

If you look through the names in your portfolio you will likely recognize all of them. You buy their products and services everyday. That does not mean these companies will not fluctuate in their value – they always have and always will. Many have historically paid dividends and increased those dividends during challenging times including WW-II, previous pandemics (the 1980 AIDS virus to current), and many other bumps along the way.

No doubt, the past month has been a wild ride. But there are lessons to be learned in all of this. Be a student of not only economics, but of emotion and behavior.

We will get through all of this. We will continue to walk this path with you.

Steve Booren is the Owner and Founder of Prosperion Financial Advisors, located in Greenwood Village, Colo. He is the author of Blind Spots: The Mental Mistakes Investors Make and Intelligent Investing: Your Guide to a Growing Retirement Income and a regular columnist in The Denver Post. He was recently named a Barron’s Top Financial Advisor and recognized as a Forbes Top Wealth Advisor in Colorado.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.