Many Americans Face a Bitter-Sweet Early Retirement. What Should They Do?

He was sitting on a bus stop bench outside a tranquil park, wearing a khaki suit, checkered blue shirt and sneakers. A plain white box rested on his lap when he greeted a stranger and offered her a chocolate saying, “My Mama always said life was like a box of chocolates…you never know what you gonna get”.

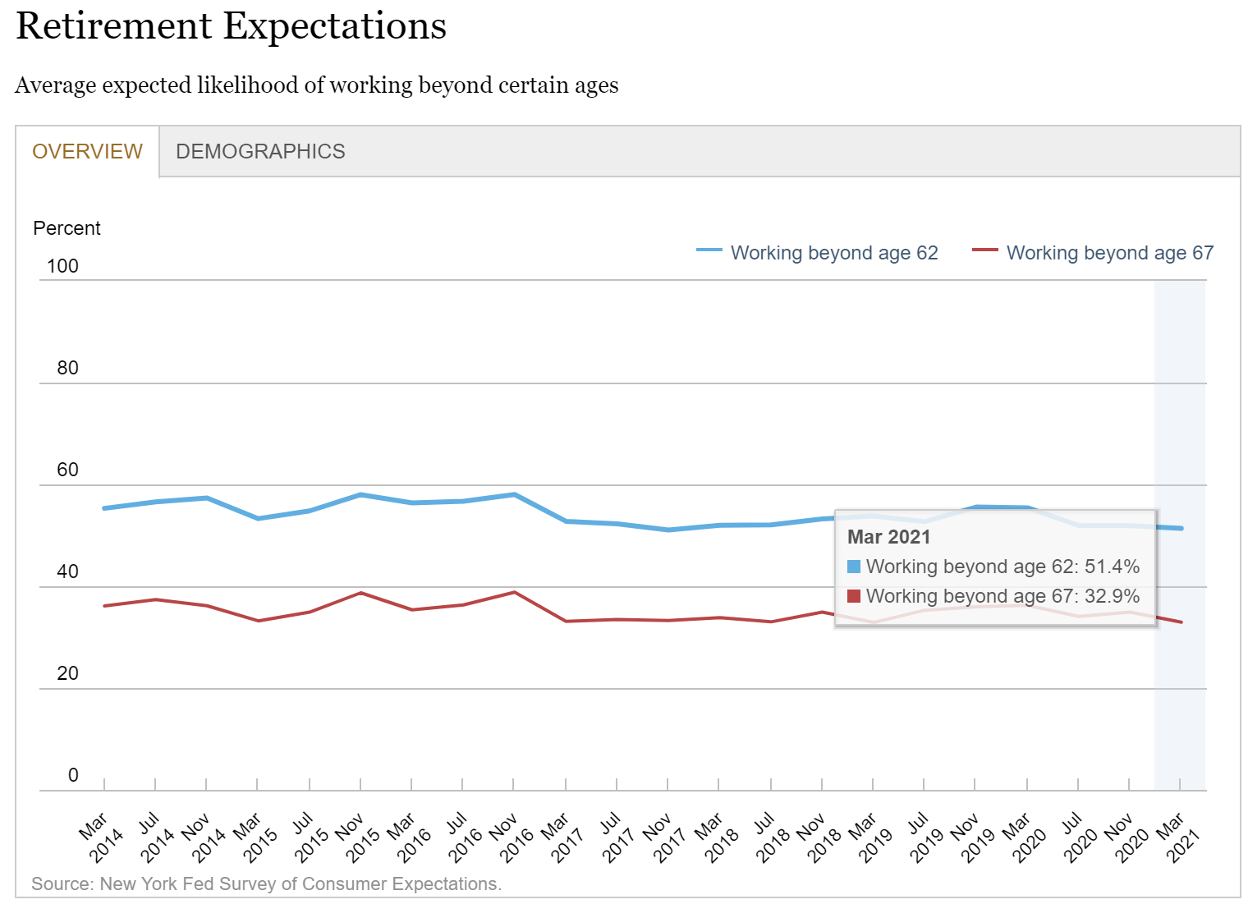

What a simple, insightful thought. Forrest Gump is one of my favorite Tom Hanks characters. There is so much we can learn from the critically acclaimed 1994 film. But that quote, reminding us that life is as much of a mystery as what flavor chocolate we will pick, comes to mind when I read about the thousands of Americans retiring every day. Many of whom are being forced to retire before they wanted. The average expected likelihood of working beyond age 67 declined to 32.9 percent in March 2021 according to a labor market study conducted by the Federal Reserve Bank of New York. The same study also indicates only a little over half of workers will work past age 62.

This trend certainly accelerated in 2020. The Pew Research Center estimates that 3.2 million more Baby Boomers retired in the third quarter of 2020 than in the same quarter in 2019. Read that again. Not 3.2 million total, but 3.2 million more. In total, 28.6 million Baby Boomers retired that quarter. That sure sounds like a lot of people – especially when our social gatherings have been under 10 people for the last year!

Sadly, many of those new retirees were not planning or even wanting to retire so soon. The pandemic made that decision for them. I feel for those folks who enjoyed their job and planned to work as long as they physically and mentally could, but were instead fed a different flavor of chocolate by factors outside their control. We will never be able to control everything in life, but there are things we can control and should focus on.

If you find yourself forced into retirement earlier than you planned, take a deep breath. You’ve been through unexpected challenges before and you will navigate this one too. Know that you do not need to navigate this transition alone! Working with a financial advisor can help you to make informed, objective decisions and provides confidence that you are controlling what you can control.

When I help clients with retirement planning, we start by looking at your net worth today. Make a list of your assets (cash savings, investment and retirement accounts and property, etc.) Next to your assets list your liabilities (mortgages, auto loans, student loans, credit card debt, etc.). Subtract the total value of your liabilities from the total value of your assets to find your net worth.

Once you have a comprehensive snapshot of your financial picture, take a closer look at your cash reserves and outstanding debt. You want to make sure you have enough cash to address unplanned expenses, but not too much as inflation will eat away your precious purchasing power. Typically, you should target maintaining the equivalent of 3-6 months of living expenses in a savings account as your Emergency Fund. However, as you approach retirement or are forced to retire you may want to consider increasing that amount to the equivalent of 6-12 months of living expenses. A larger cash buffer can help you ease the transition from a steady paycheck.

In an ideal world, you paid off your debts before retirement. In reality, many people continue to have debt beyond their working years. This is a good opportunity to review those debts to see if it makes sense to pay it down more aggressively or if you are comfortable with continuing to pay over the regular schedule remaining on the loan. If you are carrying credit card debt or high interest rate debt (think loans with a higher borrowing cost than you expect to return on your investment portfolio), you may want to target paying those debts down faster or with excess cash.

Interest rates are still historically low, so there may be an opportunity to lower your borrowing costs. However, you need to plan ahead and look to refinance before retiring, if you have the luxury of planning your retirement date in advance. You would likely find it more difficult to refinance once employment income has ended, as lenders provide financing based on consistent cash flow, as opposed to net worth.

Next, take a deeper dive into cash flow. Take the time to review your monthly expenses to create awareness about your spending. There are likely to be some changes to your spending once you are done working. For example, you may spend less on career related items such as commuting, professional clothing, etc. However, with a large increase in free time you may spend more on hobbies and leisure activities. Health insurance is another big expense that most people have through their employer. If you find yourself retired prior to 65, you may have a big cost increase coming to continue health coverage. With an understanding of your average monthly expenses you can double check that your Emergency Fund is appropriate.

Most people meet their retirement needs from a combination of sources, including investment income, Social Security, employer pensions and part time work. Loss of purchasing power is one of the greatest and most overlooked risks to retirement. To protect yourself from this risk your income should be growing faster than the inflation rate. An effective approach is to invest in companies that pay and consistently grow their dividends. Historically, the growth rate of dividends can outpace the inflation adjustments on Social Security and pension benefits (if your pension even adjusts for inflation). Since 1990 the average dividend growth for the S&P500 is 5.89%, while the average cost of living adjustment for Social Security is 2.36%

Still, Social Security is a key retirement income source for many people. When to claim benefits is a decision within your control. It is important to put thought into when it makes the most sense for you to claim benefits, as opposed to simply claiming when you retire. Factors including your life expectancy, income needs, desire to pursue new work opportunities, and earnings history all play into what makes sense for you. Your Social Security benefits are based off your highest 35 years of earnings, so I suggest reviewing your earnings history to see how many years you have accumulated. If you have less than 35 years, it could be worth finding a new job, even part time, as even a smaller amount of income would replace a year of zero earnings and help boost your benefits.

With your net worth and cash flow buttoned up, there is one more essential consideration: You! Retirement, planned or forced, represents a major life transition. Spend time reflecting on how you will remain engaged, find purpose, and fill your days. You have an opportunity to spend more time with family, engage your community in new ways, develop hobbies or work part time at a job you enjoy. If you’re at a loss for ideas, maybe start by watching Forrest Gump; he sure had a wide variety of life pursuits! However you choose to do it, staying active bodes well for your physical and mental health. All the time spent considering your finances will have been for not if you fail to care for yourself.

When it comes to retirement planning and life, focus on what you can control. As Forrest Gump said, “You have to do the best with what God gave you.” Remember, don’t be afraid to ask for help. Your Financial Advisor can help you maximize how your resources serve you. I hope the next stage of your life is as sweet as it can be.

Sources:

https://www.newyorkfed.org/microeconomics/sce/labor#/expectations-retirement1

https://www.ssa.gov/oact/cola/colaseries.html

https://www.multpl.com/s-p-500-dividend-growth

Hello! I am Danny Kellogg, an LPL Financial Advisor with Prosperion Financial Advisors. The best part about my job is using my experience and education to help clients discover how their financial resources can serve them. To deepen my knowledge and demonstrate my dedication to serving clients at the highest level, I became a CERTIFIED FINANCIAL PLANNER® and Retirement Income Certified Professional®. My wife Elizabeth and I are both proud Colorado natives. We live in Centennial, CO with our daughter Libby and golden retriever Aggie. I am an avid Colorado sports fan who enjoys cheering on the Rockies, Broncos, Avalanche, Nuggets and Colorado State University Rams. When I am not helping clients, I enjoy spending time with my family and playing golf.