Tag Archive for: Business Owners

https://prosperion.us/wp-content/uploads/2026/06/innovation.jpg

1001

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2026-06-22 12:51:252026-06-22 12:51:25Automation + Innovation = Transformation

https://prosperion.us/wp-content/uploads/2026/06/innovation.jpg

1001

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2026-06-22 12:51:252026-06-22 12:51:25Automation + Innovation = Transformation https://prosperion.us/wp-content/uploads/2026/05/first-monday-of-retirement.jpg

735

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2026-05-05 15:12:212026-05-05 15:15:22The First Monday of Retirement

https://prosperion.us/wp-content/uploads/2026/05/first-monday-of-retirement.jpg

735

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2026-05-05 15:12:212026-05-05 15:15:22The First Monday of Retirement https://prosperion.us/wp-content/uploads/2026/04/money-value-of-time.jpg

800

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2026-04-20 10:41:292026-04-20 10:41:29The Money Value of Time

https://prosperion.us/wp-content/uploads/2026/04/money-value-of-time.jpg

800

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2026-04-20 10:41:292026-04-20 10:41:29The Money Value of Time https://prosperion.us/wp-content/uploads/2025/11/checklist.jpg

467

1000

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-11-18 12:17:442025-11-18 12:25:46Preparation Over Panic

https://prosperion.us/wp-content/uploads/2025/11/checklist.jpg

467

1000

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-11-18 12:17:442025-11-18 12:25:46Preparation Over Panic Sketchplanations

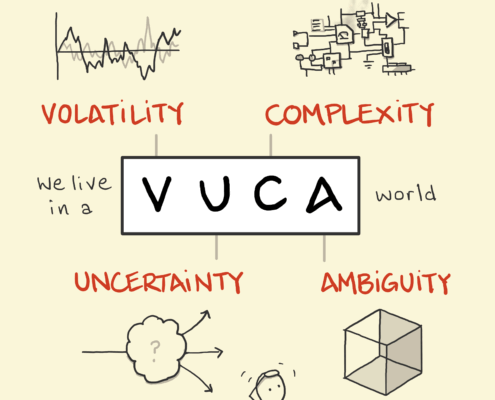

https://prosperion.us/wp-content/uploads/2025/11/sketchplanations-vuca-scaled.png

2560

2560

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-11-01 11:58:312025-11-18 12:05:17The Antidote to Ambiguity

Sketchplanations

https://prosperion.us/wp-content/uploads/2025/11/sketchplanations-vuca-scaled.png

2560

2560

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-11-01 11:58:312025-11-18 12:05:17The Antidote to Ambiguity https://prosperion.us/wp-content/uploads/2025/10/certaintyofuncertainty.jpg

1000

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-10-04 12:30:052025-10-20 12:36:05The Certainty of Uncertainty

https://prosperion.us/wp-content/uploads/2025/10/certaintyofuncertainty.jpg

1000

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

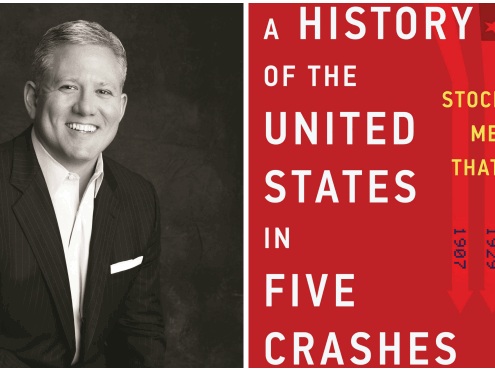

Steve Booren2025-10-04 12:30:052025-10-20 12:36:05The Certainty of Uncertainty https://prosperion.us/wp-content/uploads/2025/09/hisotry-in-5-crashes.png

373

749

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-09-23 09:33:162025-09-23 09:33:16The Telltale Signs of a Market Crash

https://prosperion.us/wp-content/uploads/2025/09/hisotry-in-5-crashes.png

373

749

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-09-23 09:33:162025-09-23 09:33:16The Telltale Signs of a Market Crash https://prosperion.us/wp-content/uploads/2025/08/Microsoft-Founded-1.jpg

600

900

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-08-18 13:08:152025-08-18 13:28:24The Bell-Bottom Billionaires

https://prosperion.us/wp-content/uploads/2025/08/Microsoft-Founded-1.jpg

600

900

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-08-18 13:08:152025-08-18 13:28:24The Bell-Bottom Billionaires https://prosperion.us/wp-content/uploads/2025/07/apple-starbucks.jpg

641

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-07-21 10:11:122025-07-22 10:12:19Don’t Just Own Shares: Share Ownership

https://prosperion.us/wp-content/uploads/2025/07/apple-starbucks.jpg

641

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-07-21 10:11:122025-07-22 10:12:19Don’t Just Own Shares: Share Ownership https://prosperion.us/wp-content/uploads/2025/06/perspective.jpg

709

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-06-17 10:11:412025-06-17 10:11:41History Over Headlines

https://prosperion.us/wp-content/uploads/2025/06/perspective.jpg

709

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-06-17 10:11:412025-06-17 10:11:41History Over Headlines https://prosperion.us/wp-content/uploads/2025/05/meeting-mr-market.png

1024

1536

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-05-20 09:47:152025-05-20 09:52:36Meeting Mr. Market

https://prosperion.us/wp-content/uploads/2025/05/meeting-mr-market.png

1024

1536

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-05-20 09:47:152025-05-20 09:52:36Meeting Mr. Market https://prosperion.us/wp-content/uploads/2025/04/awesome-less-awesome-sign.jpg

922

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-04-21 11:41:072025-04-21 11:41:07We Plan For This

https://prosperion.us/wp-content/uploads/2025/04/awesome-less-awesome-sign.jpg

922

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-04-21 11:41:072025-04-21 11:41:07We Plan For This https://prosperion.us/wp-content/uploads/2024/03/barrons-top-financial-advisor.jpg

617

1500

Administrator

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Administrator2024-03-25 10:43:302024-03-25 10:43:44PRESS RELEASE: Steve Booren Recognized as One of America’s Top Financial Advisors by Barron’s

https://prosperion.us/wp-content/uploads/2024/03/barrons-top-financial-advisor.jpg

617

1500

Administrator

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Administrator2024-03-25 10:43:302024-03-25 10:43:44PRESS RELEASE: Steve Booren Recognized as One of America’s Top Financial Advisors by Barron’s https://prosperion.us/wp-content/uploads/2023/09/fortune-telling.jpg

844

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2023-09-18 10:47:132023-09-18 10:47:13Forecasting: An Illusion of Knowledge

https://prosperion.us/wp-content/uploads/2023/09/fortune-telling.jpg

844

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2023-09-18 10:47:132023-09-18 10:47:13Forecasting: An Illusion of Knowledge https://prosperion.us/wp-content/uploads/2023/06/bondsign.jpg

678

1250

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2023-06-20 14:30:072023-06-20 14:30:07Own or Loan? Equities vs. Bonds

https://prosperion.us/wp-content/uploads/2023/06/bondsign.jpg

678

1250

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2023-06-20 14:30:072023-06-20 14:30:07Own or Loan? Equities vs. Bonds