Bullish on Humility, Gratitude, and Discipline

The CNBC Host of Mad Money, Jim Cramer, is famous for saying “There is always a bull market somewhere.”

This year it’s been challenging to remain bullish about most finances, but I have found bull markets in humility, gratitude, and discipline.

It has been a year for humility as many of the traditional methods of managing risk inside portfolios have been taxed. It has been a year of consciously focusing on gratitude for all that we have and all that has gone well. It also has been a year where the value of our disciplined commitment to planning has never been more highlighted.

There’s much to learn from reflecting on the year. It taught us, or retaught in many cases, what is true, what is meaningful, what can be counted on, and what cannot.

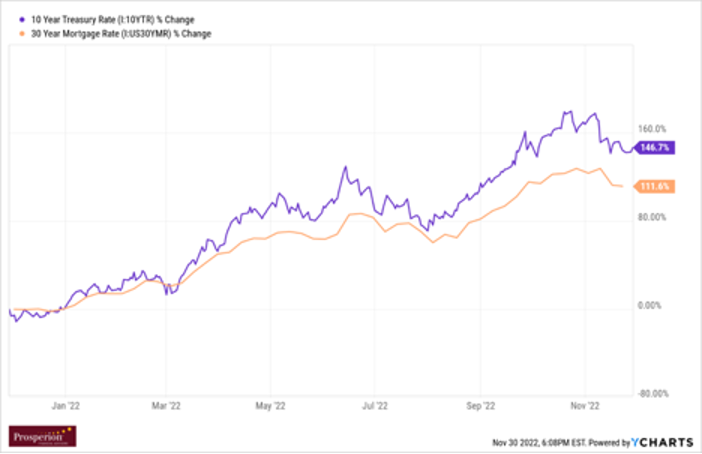

In the closing scene of Norman Maclean’s classic tale, A River Runs Through It, the Reverend McLean observed “Eventually all things merge into one and a river runs through it… I am haunted by waters”. This has been a year of many things merging into one with the river of inflation running through it. Consider the correlation of these asset classes:

Traditionally at least one, if not many of these, do well when others do poorly. This year however, they’ve been in lockstep. The one outlier is the U.S. inflation rate and the Federal Reserve’s (Fed) response to it, the river perhaps responsible for much of the correlation.

This was not completely unexpected. If we define inflation as too many dollars chasing too few goods, then COVID exacerbated both sides of that equation. On the demand side, stimulus checks, the CARES Act, hyper-low interest rates, as well as quantitative easing and lending programs, all led to a U.S. economy flush with cash. On the supply side, the US Government “shut down” the economy by encouraging non-essential workers to stay home. As it turns out, the US economy is not your kitchen light switch – it can’t be turned off and on without consequence. Those consequences, at least financially speaking, have come in the form of hyperinflation, the likes of which not seen since the late 1970s.

The Federal Reserve, dually mandated to keep unemployment and inflation low, is now challenged with the undesirable task of fixing the problem. Their most effective tool is fairly blunt: raising the Federal Funds Rate. Given that bond prices and interest rates have an inverse relationship, it makes sense that bonds are on pace for their worst year on record. What doesn’t make sense is the Bloomberg Global Aggregate Bond index is down more than the Russell 2000 index.

We have experienced and will continue to experience a major paradigm shift in market dynamics. The go-go growth days of low inflation and low interest rates are behind us for the time being, and we are living through, planning around, and investing in a new reality where growth is harder to come by, volatility is elevated, and the cost of borrowing is meaningfully higher along with the cost of living. Consider the year-to-date increase in the 30-year-mortgage rate: it’s up 111% in less than one year. Unprecedented.

This new paradigm will continue to require new ways of thinking, planning, and investing, but will not affect the core principles of success over the last several decades. When things get complicated, we go back to the basics. Core truths are the drivers of results. Here are some of the things to keep in mind.

Over Time, Markets Trend Upward

Long Term Trend

Long term perspective matters. With good planning, the noise of short-term volatility matters very little. Think about the most challenging events since 1926 – the great depression, at least 15 recessions, several wars, many global, pandemics, geopolitical turmoil and yet, the S&P 500 has returned nearly 10.5% annualized over that near 100-year period.

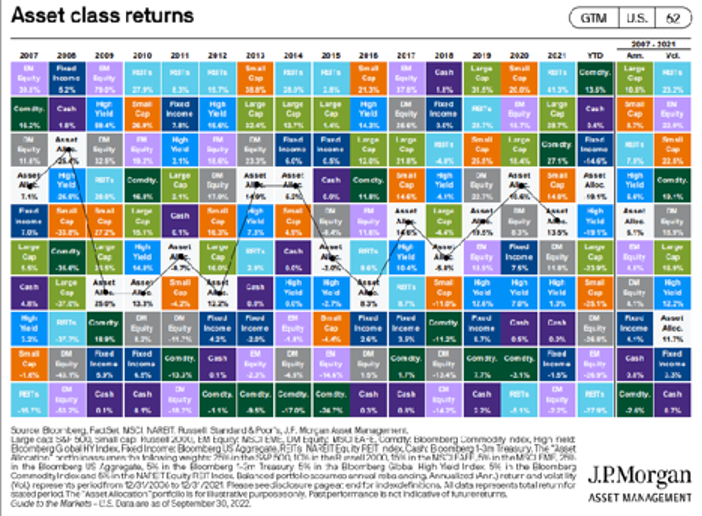

Diversification Done Well, Works Well (Babe Ruth vs. Money Ball)

In 1927 Babe Ruth broke the major league baseball record by hitting 60 home runs in a season. Lesser known than his home run record was his number of strike outs: 89 times. His ideology of “Never let the fear of striking out keep you from swinging,” is very different than the Money Ball approach made famous by Billy Beane and the Oakland Athletics in 2002. The idea behind Money Ball was about using statistical analysis to shift the odds in one’s favor. In the 2011 movie of the same name, there is a scene where all the talent scouts gather in a room to decide which players to recruit. A debate breaks out over a suggested player, David Justice, who may not be a “home run” hire. Brad Pitt turns to Jonah Hill and asks, “Why do we like him?” to which Jonah Hill replies, “He gets on base.” With diversification, we are not always hitting home runs (if we were, we wouldn’t be diversified), but we do give ourselves a good chance of getting on base and staying competitive for the long run.

“Diversification is the only free lunch in investing,” said Nobel Laureate Harry Markowitz. Warren Buffet describes diversification as “protection against ignorance.” While the above chart is NOT indicative of how our portfolios are allocated or have performed, it does highlight our belief that diversification done well, works well. It helps reduce the impact of market volatility, takes advantage of different investment opportunities, helps work toward stated long-term goals, aims to increase the benefit of compounding, and helps manage risk from singular problem areas.

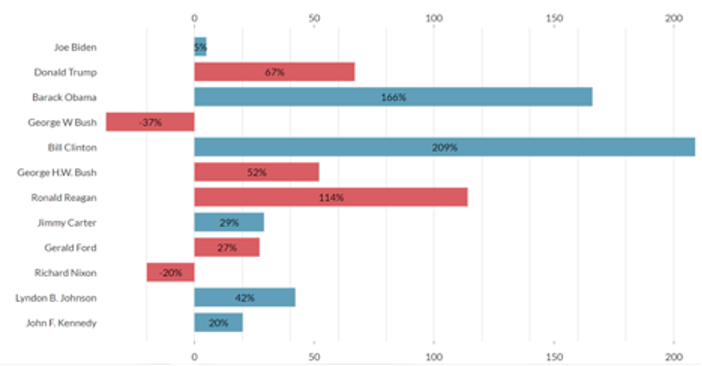

Markets Have Historically Traded Independent of Politics:

Cumulative S&P 500 Performance By President

Factsfirst.com/metrics/stock-market-performance/

In our politically charged environment, this header is important to remember, but it would be naive to think politics don’t have the ability to somewhat impact markets indirectly in the short term. Simply put, political actions, regulations, tax laws, etc. can have a short-term impact on the profitability of certain corporations, but politics is not the main driver of a company’s long-term performance. As investors we are buying equity in businesses, not in any one political party or administration. In investing, it is the outlook of the businesses that matter more than politics.

Portfolio Discipline Matters

When markets have challenging years like 2022 has proven to be, it is tempting to abandon discipline and chase what is popular in the moment. In these times we come back to our guiding principles for managing portfolios through all market cycles. Our foundational disciplines of building portfolios around financial plans, remaining diversified, playing defense, focusing on quality and liquidity, being nimble but not fragile, active tax management, and keeping a long-term perspective all matter a great deal through market cycles good and bad.

What you DON’T Invest in Matters

Avoidable pitfalls are just as important to your financial success as the “home runs” you are able to hit. Bitcoin is a classic example. We were constantly asked, even sometimes ridiculed, for not investing in bitcoin in 2020 and 2021. But we did not see a clear investment thesis in cryptocurrency and had grave concerns over its lack of regulation. Pitfall avoided.

Personalized Financial Planning Matters

Great financial planning accomplishes many things. First, it deepens your financial understanding of your whole financial picture. Second, it increases confidence. Having a plan can help decrease uncertainty, especially in volatile times, and guide you toward necessary adjustments to stay on track. Third, it informs your portfolio allocation and strategy. Fourth, it creates great wealth-building habits that apply when times are good, as well as when times are challenging. Fifth, it prepares you for unforeseen situations and emergencies.

By engaging in personalized, holistic financial planning, you reduce uncertainty and in years like 2022, risk management across your entire financial life becomes essential.

Emergency Reserves Matter

Often, if you have followed our advice and are holding an emergency reserve, it can be difficult to see this reserve as valuable. Why hold cash when inflation is double digits? Emergency reserves are a strategic asset class that allow the rest of your financial plan to weather the ups and downs of investing as you move toward your long-term goals. These dollars serve a very important role in your financial success, though sometimes it may not feel it. But not being forced to sell an asset at a loss to fund an emergency can be a huge win. Don’t be tempted to spend or invest these dollars! (Except in emergencies, of course.)

Controlling Your Spending and Savings Matters

You can’t out invest a bad spending habit on your way to building wealth. You must spend less than you earn and prudently invest the difference. The difference between what you make and what you spend is your personal profit margin. As with a corporation, the higher your personal profit margin, the better. When you actively save the difference between what you make and what you spend, you love opportunities like 2022, a chance to buy shares of ideal companies at comparatively low prices. In his 2017 Berkshire Hathaway Shareholder Letter , Warren Buffet said, “Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it’s imperative that we rush outdoors carrying washtubs, not teaspoons.”

If you are actively spending less than you make and saving the difference, 2022 is a dark cloud scenario, and the amount you are saving determines whether you are running out with a teaspoon or a washtub.

Tax Management Matters

Years like 2022 may not offer stellar returns, but they do present us with opportunities to tax loss harvest. Whenever possible and appropriate we have sought to tax loss harvest on a client-by-client basis to help offset potentially large tax burdens. A silver lining to be sure.

Other forms of tax management are vital as well. Your savings vehicle (pre-tax vs. post-tax), where you chose to withdraw funds needed for living expenses, understanding deductions for which you are eligible, and reviewing your gifting strategies all play a role in a well-managed tax plan.

What Doesn’t Matter

Investment Decisions You Made in the Past

You can’t change decisions already made and you can’t drive forward staring in the year review mirror. Learn from the past, but don’t be bound by it.

What Your Neighbor/Friend/Family/Co-Worker is Invested In

Fear of missing out leads to some grave investment mistakes. Your neighbor may have made money in dogecoin in 2021, but that does not constitute sound investment advice and mean you should blindly follow suit. Your neighbor/friend/family/co-worker/peer group all operate with a different set of values than you, different goals, time horizons, risk tolerances, and financial realities. Their plan will never be your plan. You are different people with individualized life circumstances and goals.

Having a personalized financial plan allows you to say “no” to speculative ideas and guards against the fear of missing out.

News Headlines and Fear Mongering

Fear sells. Fear gets more clicks. Fear garners more attention and contributes to higher advertising revenue. Headlines are going to be negative, don’t expect anything different. As the CEO of First Trust Jim Bowen likes to say, “Use data to shred the narrative.” Headlines don’t matter, factual data does.

Short Term Price Volatility

Volatility is the price of growth. Prices go up and down – that’s the nature of investing. If short-term price swings are causing you angst, you need to revisit your financial plan, your asset allocation, and your temperament as an investor. If all of those are adequately aligned, then short-term volatility should not matter.

Changing for the Sake of Changing

When markets are down, the temptation is to want to do something…anything! The White Rabbit in Alice in Wonderland said it best, “Don’t just do something, stand there!” Often the best course of action is to do nothing. Changing for the sake of changing has no value.

Short Term Market and Economic Forecasting

The Federal Reserve Board employs just over 400 PhD-level economists. In 2021 the Fed was first confronted with higher-than-average inflation for the first time in decades. In their assessment at that time, inflation was merely going to be “transitory.” Treasury Secretary Janet Yellen expected inflation to drop by the end of 2021, and that was the consensus of some very well-educated and highly respected economists.

Turns out even the brightest minds in finance make mistakes. In the short term, market and economic forecasting is both hard and pointless. The economy and markets are very broad and digest millions of data points from across the globe daily. It’s simply impossible to know which of those data points is going to move the needle in the short run.

In closing, while this has indeed been a challenging year – one for the record books in my opinion – I hope this article is encouraging to you. It’s easy to feel helpless in years like this, but there much you can do to keep moving forward. If you would like to discuss any of these ideas in more detail, I welcome the conversation.

It is a great honor to help you grow and steward your financial resources. Thank you for your trust. Thank you for being clients of Prosperion.

Merry Christmas and Happy New Year! May this holiday season be filled with time around those you love the most.

Brannon is a financial advisor with LPL Financial and also serves as the team’s wealth manager. He joined Prosperion Financial Advisors in 2004. In addition to being a Certified Financial Planner® (CFP) and an Accredited Portfolio Management Advisor®, Brannon has a Master’s degree in Leadership from Denver Seminary. He is passionate about helping clients make wise, informed, investment and financial planning decisions. He is married to the love of his life, Melanie, and is the proud father of his son, William. When not working with clients or spending time with family, Brannon enjoys being in the outdoors of the Colorado high country, skiing, fly fishing, and exploring wild country.