Tag Archive for: Steve Booren

https://prosperion.us/wp-content/uploads/2026/01/an-underestimated-orchard.jpg

800

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-29 11:00:122026-01-07 11:02:46The Underestimated Orchard

https://prosperion.us/wp-content/uploads/2026/01/an-underestimated-orchard.jpg

800

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-29 11:00:122026-01-07 11:02:46The Underestimated Orchard https://prosperion.us/wp-content/uploads/2026/01/markets-have-seasons.jpg

800

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-22 10:55:522026-01-07 10:59:41Markets Have Seasons—And So Does Your Portfolio

https://prosperion.us/wp-content/uploads/2026/01/markets-have-seasons.jpg

800

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-22 10:55:522026-01-07 10:59:41Markets Have Seasons—And So Does Your Portfolio https://prosperion.us/wp-content/uploads/2026/01/target-date-funds.jpg

828

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-15 10:51:502026-01-07 10:55:26The Trouble with Target-Date Funds

https://prosperion.us/wp-content/uploads/2026/01/target-date-funds.jpg

828

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-15 10:51:502026-01-07 10:55:26The Trouble with Target-Date Funds https://prosperion.us/wp-content/uploads/2018/05/tax-planning-workshop.jpg

533

800

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-08 10:47:142026-01-07 10:51:44Current Events Only Raise Uncertainty

https://prosperion.us/wp-content/uploads/2018/05/tax-planning-workshop.jpg

533

800

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-12-08 10:47:142026-01-07 10:51:44Current Events Only Raise Uncertainty https://prosperion.us/wp-content/uploads/2025/11/checklist.jpg

467

1000

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-11-18 12:17:442025-11-18 12:25:46Preparation Over Panic

https://prosperion.us/wp-content/uploads/2025/11/checklist.jpg

467

1000

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

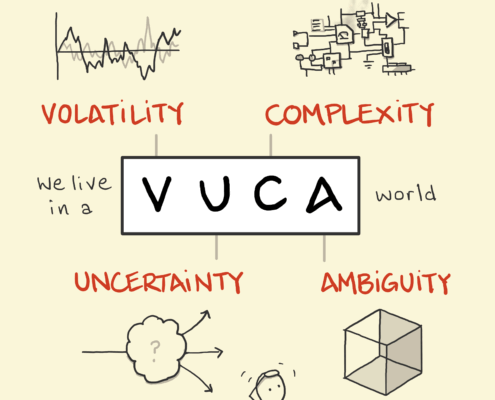

Steve Booren2025-11-18 12:17:442025-11-18 12:25:46Preparation Over Panic Sketchplanations

https://prosperion.us/wp-content/uploads/2025/11/sketchplanations-vuca-scaled.png

2560

2560

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-11-01 11:58:312025-11-18 12:05:17The Antidote to Ambiguity

Sketchplanations

https://prosperion.us/wp-content/uploads/2025/11/sketchplanations-vuca-scaled.png

2560

2560

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-11-01 11:58:312025-11-18 12:05:17The Antidote to Ambiguity https://prosperion.us/wp-content/uploads/2025/10/iphoneai.jpg

1431

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-10-20 12:28:052025-10-20 12:28:05The Price of Promise

https://prosperion.us/wp-content/uploads/2025/10/iphoneai.jpg

1431

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-10-20 12:28:052025-10-20 12:28:05The Price of Promise https://prosperion.us/wp-content/uploads/2025/10/certaintyofuncertainty.jpg

1000

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-10-04 12:30:052025-10-20 12:36:05The Certainty of Uncertainty

https://prosperion.us/wp-content/uploads/2025/10/certaintyofuncertainty.jpg

1000

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-10-04 12:30:052025-10-20 12:36:05The Certainty of Uncertainty https://prosperion.us/wp-content/uploads/2025/08/Microsoft-Founded-1.jpg

600

900

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-08-18 13:08:152025-08-18 13:28:24The Bell-Bottom Billionaires

https://prosperion.us/wp-content/uploads/2025/08/Microsoft-Founded-1.jpg

600

900

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-08-18 13:08:152025-08-18 13:28:24The Bell-Bottom Billionaires https://prosperion.us/wp-content/uploads/2025/07/apple-starbucks.jpg

641

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-07-21 10:11:122025-07-22 10:12:19Don’t Just Own Shares: Share Ownership

https://prosperion.us/wp-content/uploads/2025/07/apple-starbucks.jpg

641

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-07-21 10:11:122025-07-22 10:12:19Don’t Just Own Shares: Share Ownership https://prosperion.us/wp-content/uploads/2025/06/perspective.jpg

709

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-06-17 10:11:412025-06-17 10:11:41History Over Headlines

https://prosperion.us/wp-content/uploads/2025/06/perspective.jpg

709

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-06-17 10:11:412025-06-17 10:11:41History Over Headlines https://prosperion.us/wp-content/uploads/2025/05/meeting-mr-market.png

1024

1536

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-05-20 09:47:152025-05-20 09:52:36Meeting Mr. Market

https://prosperion.us/wp-content/uploads/2025/05/meeting-mr-market.png

1024

1536

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-05-20 09:47:152025-05-20 09:52:36Meeting Mr. Market https://prosperion.us/wp-content/uploads/2025/04/awesome-less-awesome-sign.jpg

922

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-04-21 11:41:072025-04-21 11:41:07We Plan For This

https://prosperion.us/wp-content/uploads/2025/04/awesome-less-awesome-sign.jpg

922

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-04-21 11:41:072025-04-21 11:41:07We Plan For This https://prosperion.us/wp-content/uploads/2025/03/Charlie_Munger_2.jpg

740

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-03-17 14:17:272025-03-17 14:17:27A Study in Curiosity, Simplicity, and Gratitude

https://prosperion.us/wp-content/uploads/2025/03/Charlie_Munger_2.jpg

740

1200

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2025-03-17 14:17:272025-03-17 14:17:27A Study in Curiosity, Simplicity, and Gratitude https://prosperion.us/wp-content/uploads/2024/12/clock-on-mantle.jpg

781

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2024-12-16 10:24:272024-12-16 10:24:27We Planned for This

https://prosperion.us/wp-content/uploads/2024/12/clock-on-mantle.jpg

781

1500

Steve Booren

https://prosperion.us/wp-content/uploads/2017/02/whitelogosized.png

Steve Booren2024-12-16 10:24:272024-12-16 10:24:27We Planned for This