The Power of Growing Dividend Income

We create and communicate ProsperOn’s to deliver timeless, valuable wisdom to our clients, with the hope to provide greater clarity, capability and confidence. In other words to help people be better investors. We hope these are valuable to you and your family.

By now most of you have heard us preaching the gospel of our Growing Dividend Strategy. At the very core of our investing philosophy is the notion that our clients invest for income. That income may be for today, or needed sometime in the future. But the crux is almost always income.

A focus on income invites unique challenges and opportunities. For instance, the largest challenge is a continually growing income that outpaces inflation, the “consistent hill” that always needs climbing. Without growing income the purchasing power of your money will decrease over time, along with your standard of living.

The lack of growing income has the effect of getting poor slowly. You won’t notice this on your monthly statement, or on your annual statement of net worth, but when you’re at the grocery store or kitchen table and realize your money just doesn’t go as far as it used to. That is the cancer of inflation. It shows up in the most un-expected places, un-expected times, un-announced, un-welcome, and you feel it.

Fortunately we think we’ve found a method and investment strategy designed to help overcome that obstacle, one that doesn’t involve drawing down your portfolio at an ever-increasing rate. Our method relies on the structure of one very common investment – solid companies with a history of growing their dividends at a rate of 7-10% per year.

That is why we stress to our clients the investment strategy can be explained in three simple sentences:

- We own companies that sell essential products and services, which people buy every day.

- These are companies that currently make a nice profit and share it with owners in the form of a dividend.

- The dividend has historically increased by (an average of) 7-10% per year or more generally for the past 5-10 years. 1

Compared to the more “exotic” financial plans that may be offered by the sea of sameness – the large investment brokers, insurance companies and banks, this strategy is surprisingly simple. But it helps us seek to accomplish our goal of long-term rising income. Clients are free to spend income generated from the portfolio without touching the principal or depleting a certain percentage of the portfolio. This is fundamentally different from the approach some financial advisors preach.2

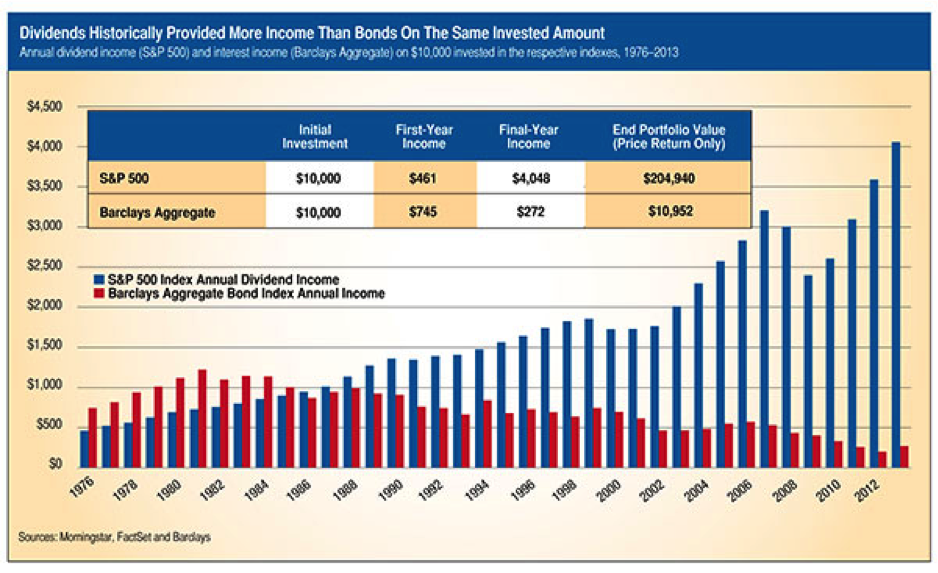

A picture tells a thousand stories; here is a revealing chart provided by Morningstar, Factset, and Barclay’s.

Past performance is no guarantee of future results. All indices are unmanaged and cannot be invested into directly. This is a hypothetical example and is not representative of any specific investment. Your results may vary.

The chart illustrates the income generated from a $10,000 hypothetical investment from 1976-2013, a 37 year timeframe. Why 37 years? Think about how long retirement lasts – don’t you want your money to last as long as you are retired? Statistically speaking for a couple retiring at age 60, it is more than likely that one of the two live in to their mid-90s. Your money and purchasing power needs to keep you covered for a long time. If not, your money runs out before you do – not a pleasant thought.

The bar chart illustrates income from the bond market in red, (benchmarked by the Barclay’s Aggregate Bond Index, something well accepted by LPL Financial and other financial services providers.) The income from dividends from the S&P 500 index are shown in blue.

Interestingly income starts out higher in the bond investment, around $745. But as interest rates have gone up and down, that income has fluctuated dramatically, and over this timeframe has decreased to the $275 range today. Conversely, income from dividends started out in the $460 per year area, steadily increasing over the timeframe, and ending at about $4,050, an increase of ten-fold. That is growing income.

What an interesting perspective: bond prices tend to be steady but the income from bonds fluctuates dramatically. Conversely, stock prices fluctuate, but the income rises steadily. Since you cannot have both, which would you rather have: rising income or steady prices, which after inflation, actually lose purchasing power?

Dividends are not guaranteed, but neither is interest from a bond. The security of those interest payments is only in the quality of the bonds you may invest in – the same can be said of dividends.

Of particular interest but not noted on this chart, inflations was up “only four fold” over this time frame.3

Our point is this: without growing income surpassing the inflation rate, investors are slowly and quietly losing purchasing power until it is too late.

In the entire spectrum of financial assets, only one has demonstrated an income that (at least since 1926) has never failed to increase at a greater rate than the CPI cost of living over 30-year time horizons. That’s why we place such value on the constantly rising dividends of great companies in America and the world.

In the past investors and advisors focused on current income or current yield. I believe this methodology and strategy has its drawbacks, and will be especially telling over a “normal retirement lifespan” of prospective retirees today.

If you would like to have a conversation about the concept of growing income with Growth of income dividends, feel free to let us know.

Thank you for being a client of Prosperion Financial Advisors.

Steve Booren is the Owner and Founder of Prosperion Financial Advisors, located in Greenwood Village, Colo. He is the author of Blind Spots: The Mental Mistakes Investors Make and Intelligent Investing: Your Guide to a Growing Retirement Income and a regular columnist in The Denver Post. He was recently named a Barron’s Top Financial Advisor and recognized as a Forbes Top Wealth Advisor in Colorado.

No strategy ensures success or protects against a loss. Stock investing involves risk including potential for loss of principal.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.