Back to Basics – 5 Investing Principles

If January taught us anything, it was that 2013 was truly an exceptional year for the equity market averages. Falling uncertainty, solid corporate earnings, and a rebounding economy all contributed to rising stock prices and exceptional performances for many portfolios. But as we’ve seen so far this year, 2014 could be more difficult. With that in mind, I think it’s a good time to return to basic investing principles, five of which I’ve outlined below.

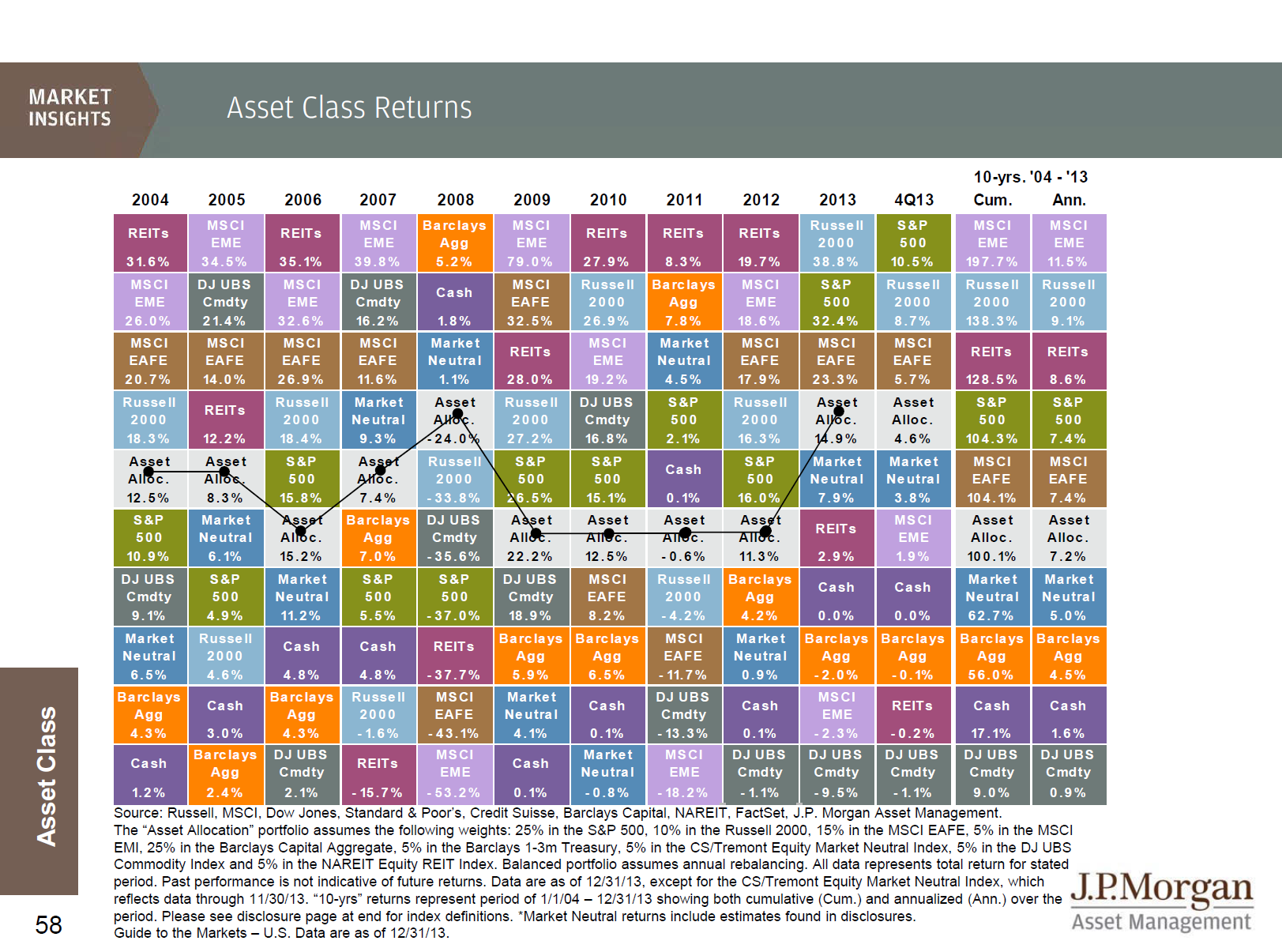

1. Have a Balanced Approach – and Periodically Rebalance

This colorful table from our research partners at J.P. Morgan illustrates the various performance of a variety of asset classes. If we knew which colorful square was going to be on top this year, investing would be easy! The problem is we have no idea! A wise investment approach is to build a balanced portfolio to match your goals and objectives, then periodically review and rebalance your portfolio to work toward meeting those needs.

2. Invest for Income, Not Yield

We believe income is the only worthwhile reason. Typically this income is either for today (during retirement for example) or for income in the future (as in saving for retirement). Furthermore, this income should be seeking growth at a rate higher than inflation to avoid the “getting poor slowly” effect of losing purchasing power. Imagine living today on the same income you made 30 years ago. This is the effect fixed income can have on investors – it is by definition “fixed”.

We believe a wise strategy is to invest in great companies that pay investors in the form of dividends, while seeking to grow those dividends systematically. This is growing income or as we have called it, a Growth of Dividends strategy.

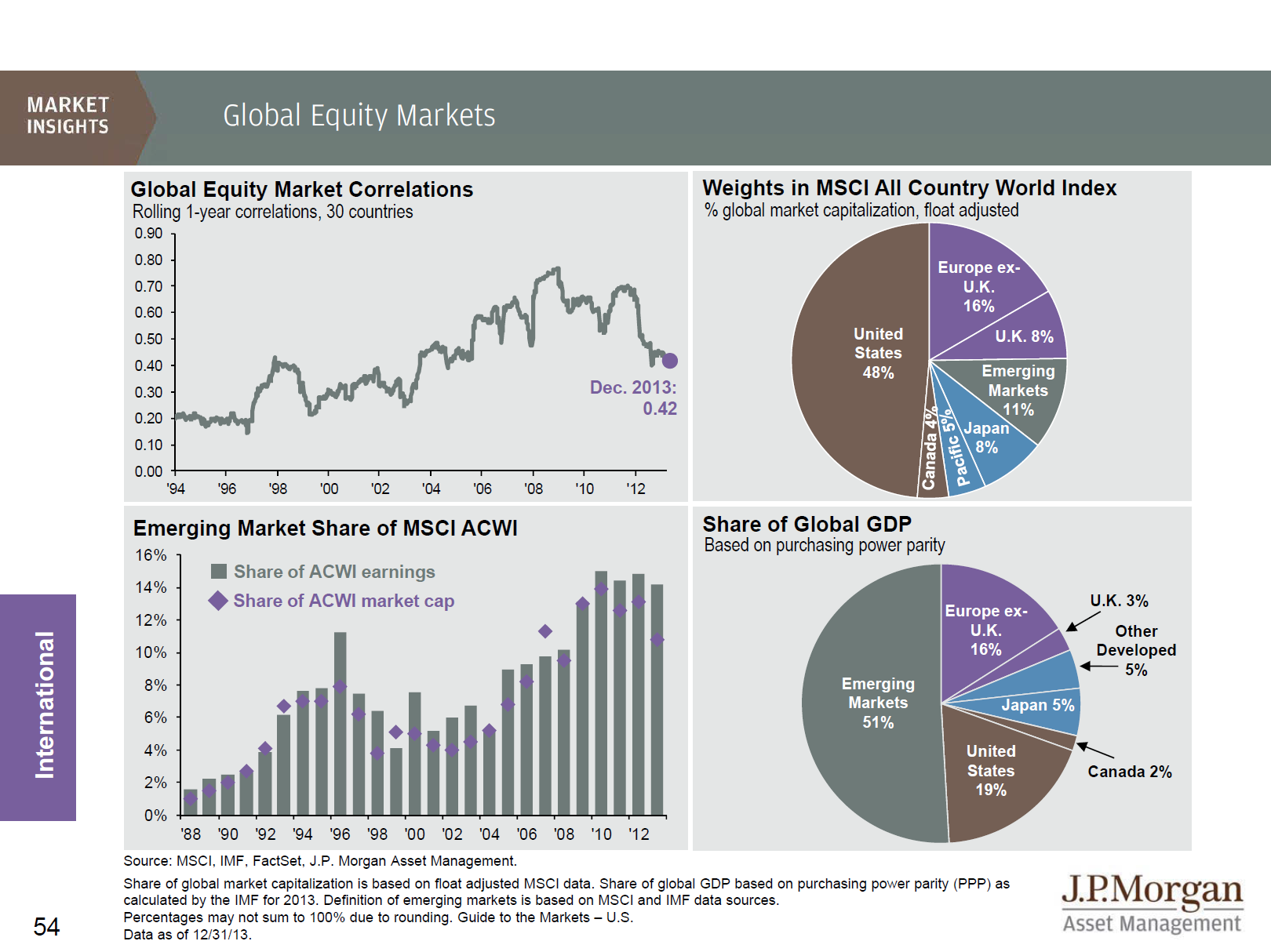

3. Diversify in Our Global Economy

Our economy is global so it makes sense to be invested in a global perspective. As you see from the Global Equity Markets, 48% of the world’s market cap is based outside the US, yet the US accounts for only 19% of the world’s GDP. We think there are really only two methods to invest globally, global markets or global companies.

Disclaimer: International and emerging market investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

With global markets, you could pick investments in far off places and markets with constantly shifting rules and regulations (as demonstrated by the disclaimer above). Or, you could invest in great global companies listed in the U.S. that sell their products around the world. Personally I think the latter is the only worthwhile option.

4. Logic Should Always Trump Emotion

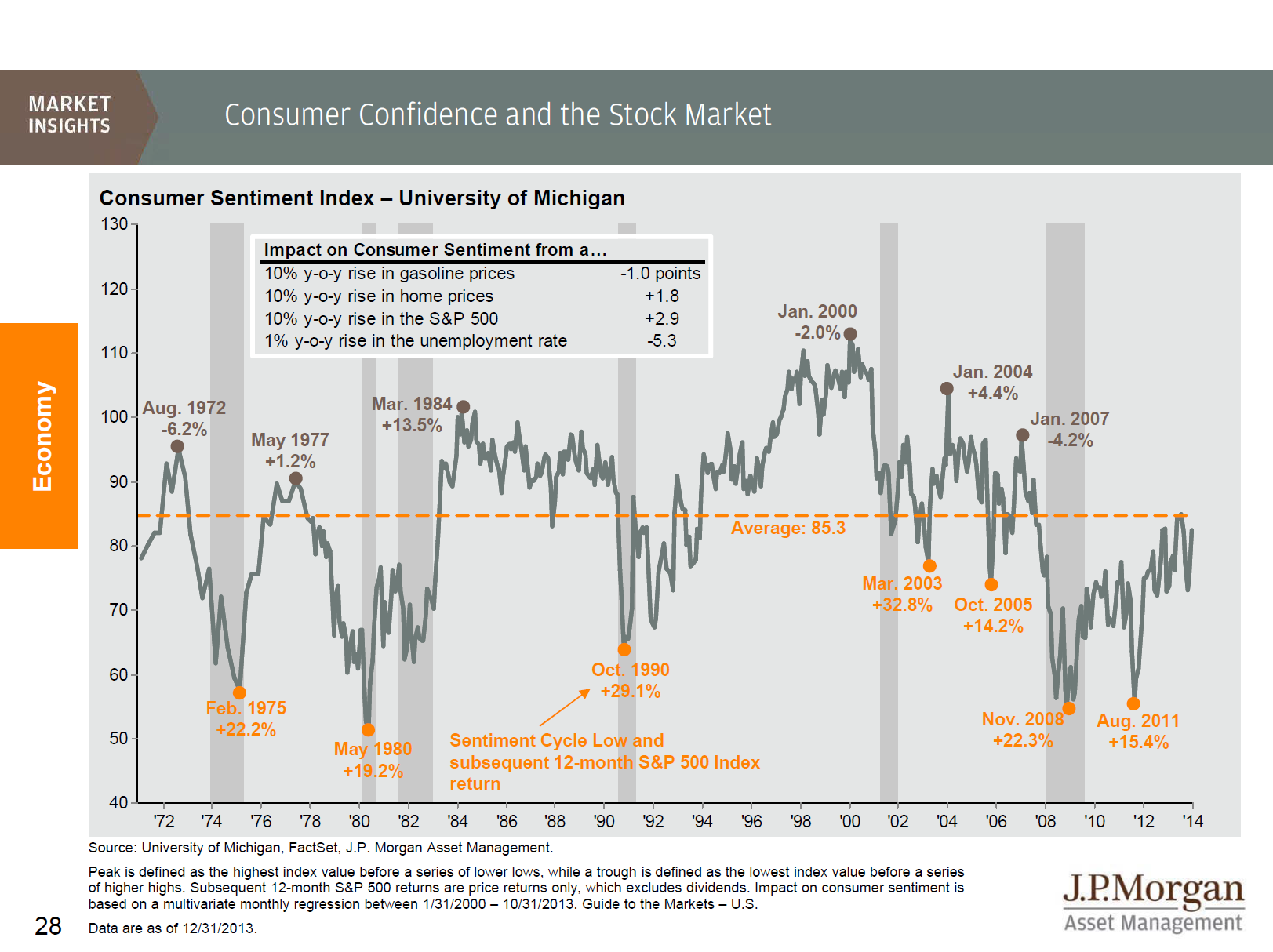

As depicted in this Consumer Confidence and Stock Market Chart, when consumer confidence is low, it usually signals a potential buying opportunity. It may sound counterintuitive, but it is true: investors should be happy when equity prices are down – it may be a potential opportunity to get great stocks. (It is important to note that just because the price of a stock is down, it does not mean that it will ever increase again. Careful selection is necessary.)

Likewise, it is odd that investors are happy when prices are high, and rising. This is akin to going to the grocery store, buying three cans of tuna for $10 this week, and next week hoping the prices will rise so you can only by two cans for the same $10. Think about that. The best time to buy something is when it is on sale. The disadvantage comes from never knowing when the sale will happen, or if a better sale will happen later in the week. This is the equivalent of trying to time the market, and it’s often left people missing out on a great price in an effort to predict the unknown.

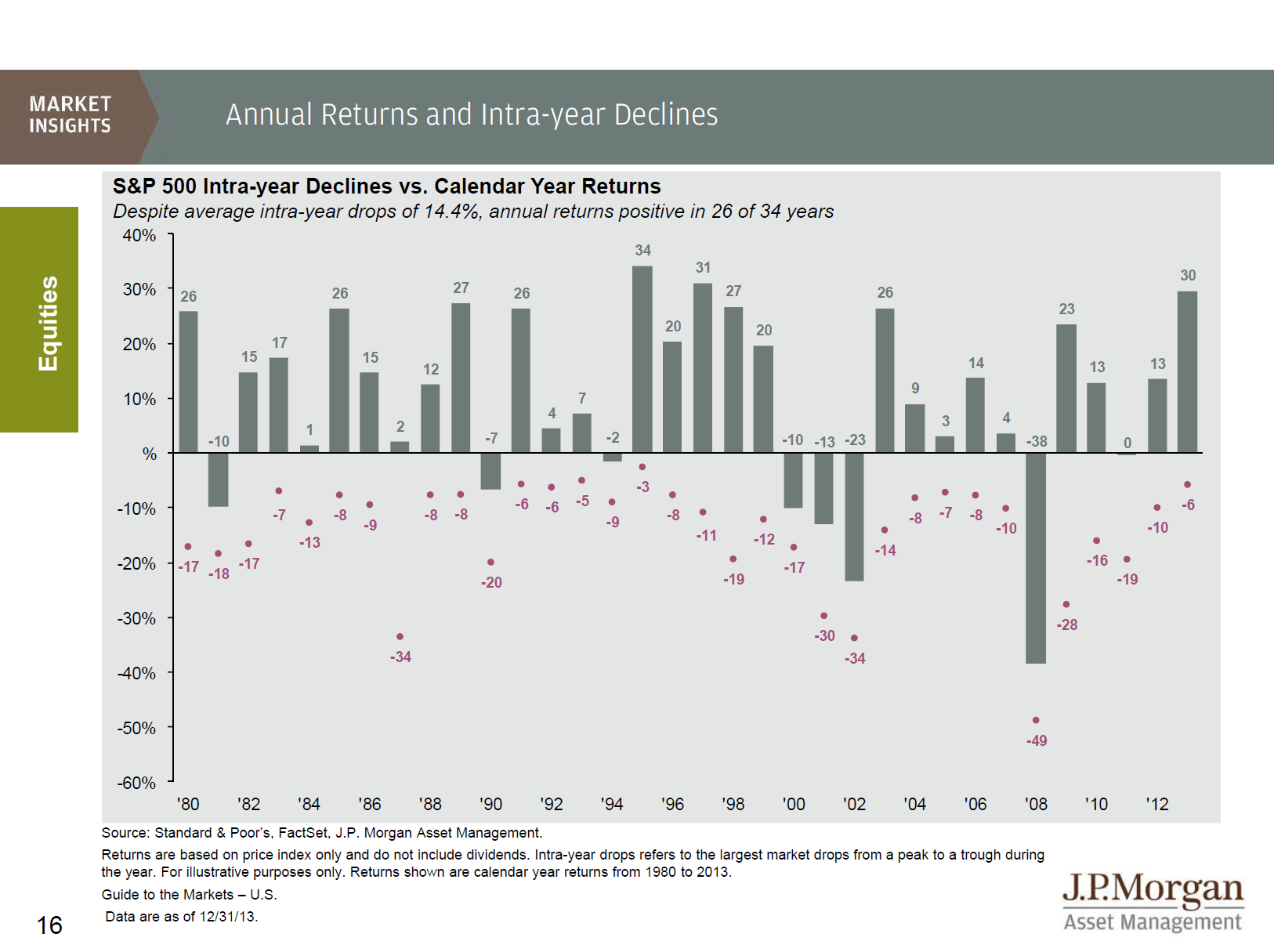

Here is another great chart that illustrates how emotion can ruin a great return. For 26 of the last 34 years, the S&P 500 has finished with a positive return, despite it being down at some point every year. Had investors sold in a panic when the market was down, they might have missed the gains realized for those who stayed invested.

5. Follow the Cash

Finally, it is valuable to look at the amount of cash still on the “sidelines”. As measured by J.P. Morgan, the total amount of cash in American households is over $10.7 Trillion. With 330 million men, women and children in America, that is about $32,700 per person – all of which is earning essentially zero percent interest. This cash is quickly losing its purchasing power due to inflation. At some point I believe some of that cash is going to find its way into a better investment as confidence returns. America is awash in liquidity – that’s not the problem. Lack of confidence is the problem, and it will return.

In Conclusion

We urge our clients to make wise choices with their money and to turn down the volume of noisy media. We encourage them to be logical, be wise and be diversified. If you or someone you know doesn’t already have an advisor, consider finding one. They can help investors avoid common mistakes like inadvertently trying to time the market or missing out on some global exposure in a portfolio.

We welcome your questions and comments. Let us know if you would like to have a conversation about these principles. We are grateful to serve as your advisor.

Steve Booren is the Owner and Founder of Prosperion Financial Advisors, located in Greenwood Village, Colo. He is the author of Blind Spots: The Mental Mistakes Investors Make and Intelligent Investing: Your Guide to a Growing Retirement Income and a regular columnist in The Denver Post. He was recently named a Barron’s Top Financial Advisor and recognized as a Forbes Top Wealth Advisor in Colorado.

Securities and Advisory Services offered through LPL Financial. Member FINRA/SIPC.

Sources:

Charts and graphs courtesy of J.P. Morgan and their Guide to the Markets 1Q | 2014