Improving Investor Behavior – Campbell’s Soup & Rising Income

Cold winter weather means it is soup season here in Colorado, and none feel more familiar than Campbell’s Tomato Soup. Just the name conjures a familiar aroma, a warmth in your chest.

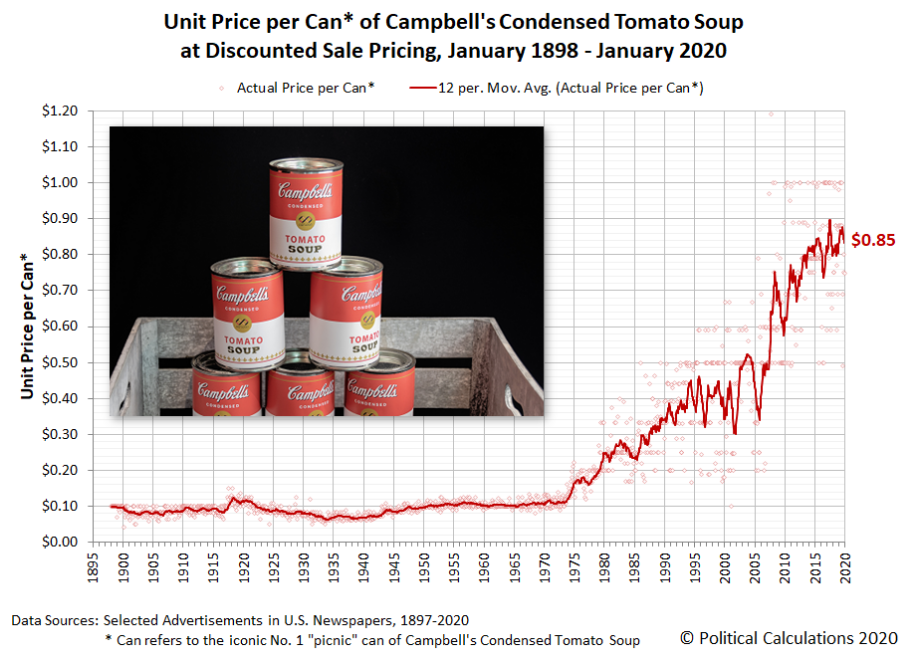

Campbell’s feels familiar because it’s been an American icon for more than a century. Introduced in 1898, Campbell’s tomato soup is an excellent benchmark for understanding the impact of the persistent enemy of all investors: inflation. For more than 100 years, the size hasn’t changed, but the price sure has. About 45 years ago, in 1974, the soup cost about $0.12 per can. Today, it retails for about $0.87 per can. That points to an average inflation rate of 4.3 percent.

Forty-five years may sound like a long time, but that’s about the length of a typical retirement. Today a 65-year-old non-smoking married couple has a 90% probability of one person reaching age 90. With innovation in healthcare, medical services, and a more active retiree base, I believe this life expectancy number will only increase.

A longer life points to a longer retirement, which in turn means a need for more assets to prevent you from “running out.” Simply said, if your income is not growing at a rate higher than inflation, you are losing purchasing power. You are getting poor slowly. The sign for this is when people say, “My income just does not go as far as it used to.” Over time prices keep rising, and your income doesn’t. This reality hits people later in life, often when it’s too late.

Consider these examples comparing common goods from 1974 to today:

|

Example Goods |

1974 |

2020 |

Avg. Inflation/Year |

|

Campbell’s® Tomato Soup |

.12 |

.87 |

+4.30% |

|

1 Dozen Eggs |

.78 |

3.68 |

+3.51% |

|

McDonald’s Quarter Pounder® |

.55 |

3.79 |

+4.28 |

|

Package of Oreo Cookies |

.55 |

3.00 |

+3.75% |

|

Kellogg’s® Corn Flakes® |

.43 |

3.29 |

+4.52% |

The problem is simple: over time, things get more expensive. Soup is one simple example, but other areas are more concerning. Healthcare, housing, education – all have seen significant increases in cost.

What’s an investor or retiree to do? That’s actually two questions. First, what do they usually do? Second, what should they actually do?

Typically, investors follow an old adage of pouring money into fixed income as they age, believing that “fixed” is good. Fixed feels stable; fixed feels safe. But it is not. Consider this: Over the last ten years, corporate earnings of the S&P 500 have risen from $83.77 in 2010 to approximately $162, close to doubling. During that same period, U.S. household investors have been net sellers of stocks and net buyers of bonds. Investors have been liquidating stocks that are increasing in value while adding to fixed income investments that pay multi-decade low rates of return. That means they’ve been trading growing income for fixed income, precisely the opposite of what they should be doing!

Over these ten years, dividend income has risen 2.6 times from $22.65 to $58.80, while the government’s official inflation rate (the CPI) has risen 19 percent. For the first time ever, senior analysts at the Dow Jones Indices expect dividend payments to exceed $500 billion, an increase of 6.4 percent in 2020. Think about this…one-half a trillion dollars being paid to investors in 2020!

Over these ten years, dividend income has risen 2.6 times from $22.65 to $58.80, while the government’s official inflation rate (the CPI) has risen 19 percent. For the first time ever, senior analysts at the Dow Jones Indices expect dividend payments to exceed $500 billion, an increase of 6.4 percent in 2020. Think about this…one-half a trillion dollars being paid to investors in 2020!

Imagine the couple who retired ten years ago and how happy they must be. Their income is up 2.6 times and their capital has nearly tripled. The fact that their capital nearly tripling is irrelevant as you do not spend your capital. The value of your account statement is an emotional “happy” or “sad” feeling as you don’t spend the balance – you spend the income earnings off your balance.

Earlier this month, fellow Denver Post columnist Charlie Farrell wrote of the investment bubbles that may be brewing, pointing out how some companies, namely technology companies, are getting “expensive.” We concur with this cautious viewpoint, which is why we focus on selecting and owning specific companies with rising dividend income rather than investment in products such as index funds, mutual funds, or ETFs that may have exposure to these over-priced companies. Funds are often incentivized to own these high-flying and expensive companies in their portfolio based on a driving force: returns. This approach works when prices are rising but is dangerous when prices begin to fall.

Indexes are “capital weighted,” in other words, they have higher allocations of the “high-fliers” which concentrates more risk in the investment. For example, the three trillion-dollar companies make up a higher percentage of the S&P than the small ones. Apple (5%), Microsoft (4.8%), and Amazon (2.89%) have a more dramatic impact on the index compared to Harley Davidson (.02%), Nordstrom (.015%) and Under Armour (0.13%). Many on Wall Street point out that these larger companies are rather expensive versus others. You should educate yourself on the risks that you are taking and understand what this means.

Farrell noted that bonds, currently at multi-decade low yields, are likely in a similar bubble. We agree that bonds at today’s interest rates represent one of the riskiest investments available.

Another way to look at this is what we call the earnings yield or owner earnings. If you owned the entire S&P 500, what would you earn on your money divided by the price? Today the earnings yield of the S&P 500 is 5.4 percent (excluding dividends). Compare this to a ten-year Treasury Bond at 1.51 percent. You could choose to have a broad portfolio of the world’s greatest companies incentivized to improve, grow, compete with one another and be better tomorrow than today. Or, you can loan your money to the U.S. Government and earn a flat return for the next ten years. It seems like an easy choice.

Earnings, income, and price are very important to understand as you invest your capital. Growing your income over a long period, such as retirement, is essential to maintaining your purchasing power. Don’t be distracted by myths of what is risky and what is not, nor those who attempt to “time” the market. It can’t be done. Understanding how these three variables work together is essential. Speak with your financial advisor and have them educate you on how this impacts your investment portfolio, your strategy, and your retirement future.

Be an informed investor with good behavior. Invest for growing income. You don’t want to find out too late that you’re not able to enjoy a bowl of Campbell’s tomato soup during your retirement.

Steve Booren is the Owner and Founder of Prosperion Financial Advisors, located in Greenwood Village, Colo. He is the author of Blind Spots: The Mental Mistakes Investors Make and Intelligent Investing: Your Guide to a Growing Retirement Income and a regular columnist in The Denver Post. He was recently named a Barron’s Top Financial Advisor and recognized as a Forbes Top Wealth Advisor in Colorado.