When Will the Market “Correct”?

March 9th, 2015 marks the sixth anniversary of the end of the last market correction. That day the Standard & Poor’s 500 ended at 676.53 versus today’s closing level of 2,100. But the significance of the sixth anniversary is not one of value, but of time and the frequency of bear markets.

Historically there have been 14 bear markets in the 70 years since WWII. Do the math and this works out to be one every five or so years. Looking at the calendar, it seems we are overdue for our scheduled correction. But unlike the dentist, the market doesn’t schedule an appointment with investors a year in advance. As a result we’re not sure when our checkup is due, but I believe we can be certain of two things:

- It is surely coming at some point.

- People will wager their retirement in an effort to time the market, likely missing the top and bottom while managing to underperform the market overall.

It has been my experience that those who try to time the market typically end up worse off than if they had just stayed the course. Market volatility is something we neither are able to control nor predict. What we can control is how we react and respond to it. In my view declines are always temporary while advances are more permanent. History provide many examples.

The night before the first decline in May of 1946, some 14 corrections ago, the S&P 500 peaked at 19. Today it is around 2,100. The dividend in 1946 was around $0.70, in 2014 it was $39.44 (up 56 fold versus inflation as measured by the CPI up less than 13 fold). This furthers my belief that investing is a long term proposition, and investing in a portfolio focused on growing dividend and growing income investments can help protect your purchasing power.

But that doesn’t stop some investors from trying. Some resort to just two things, a calendar and the overall returns of the market. Both of which are nonsense. Going back to all the bear markets since 1926, the average time from a peak to a trough and back is 3.3 years or around 40 months. The 14 bear markets since 1946 ranged from -19% to -57% from peak to trough, averaging -31%.

If you exit the market when it is “officially in a bear market”, or -20%, on average 2/3 of the decline are already behind you, selling late. Then comes the decisions to buy back in, usually with the same false readings, buying late. This vicious cycle can destroy a portfolio in no time.

So, what should investors expect? Historically portfolios have substantial setbacks on average every five years. It is entirely predicated on investor’s ability to ride out these temporary declines that will determine if they enjoy the upswing that typically follows.

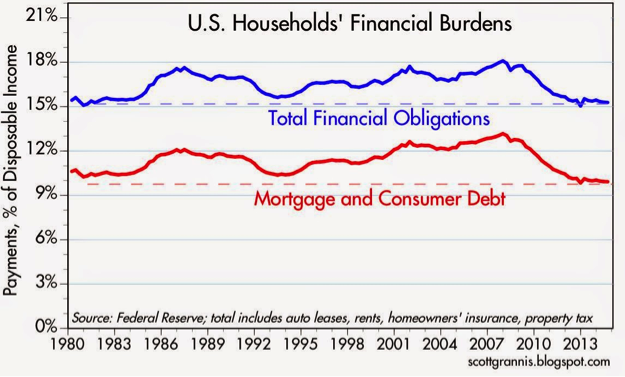

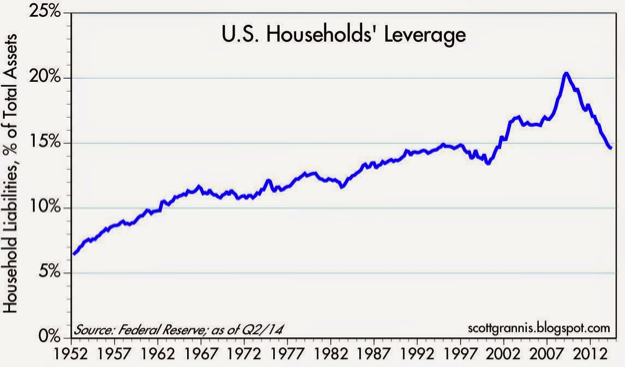

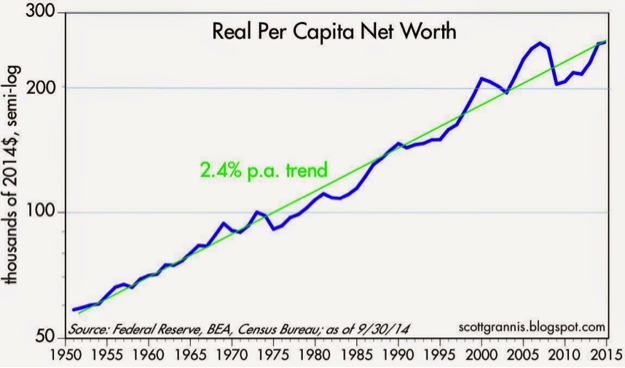

So how should we be looking at the economy, investors and investments? The American economy is expanding. Once again, we are the growth engine of the world. I believe dollar denominated assets are an attractive place to invest right now. Bull markets do not necessarily end when valuations are slightly above long term averages, as they are today. Instead it’s been my experience that they usually end when we are in a “performance at all cost” investor mentality. I just don’t see this happening. Consider these three charts that illustrate consumers and investors have de-levered, and have de-risked their balance sheets:

You can see from this first chart that investor’s financial obligations, mortgage and consumer debt levels have fallen since 2008:

And from this chart, overall investor household leverage has fallen:

And real per-capita net worth has recovered and is right in line with the historic growth rate:

In conclusion, episodes of volatility are uncomfortable, but normal. It’s the price we all pay to be a part of the American economy. But instead of fearing the inevitable, plan for it. When the time comes, keep a level head and stick to the plan. It’s the best way to keep your future on course.

We welcome any questions or a conversation regarding your progress and portfolio.

Thank you for being a client of Prosperion Financial Advisors.

Steve Booren is the Owner and Founder of Prosperion Financial Advisors, located in Greenwood Village, Colo. He is the author of Blind Spots: The Mental Mistakes Investors Make and Intelligent Investing: Your Guide to a Growing Retirement Income and a regular columnist in The Denver Post. He was recently named a Barron’s Top Financial Advisor and recognized as a Forbes Top Wealth Advisor in Colorado.

Investing involves risk including potential loss of principal. The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Sources:

Inspired by: The End of The World, Six Years On, 03/01/2015, Nick Murray