What will your income be during retirement, and will it grow with you?

This might be the single most important question you face as a pre-retiree. Many financial advisors would have you focus on the value of your portfolio, but we take a different approach.

Two Questions Every Investor Should Ask Themselves

1. What is your plan for income in the future?

2. How will that income grow with you?

Two guiding principles align an investment strategy that answers those questions

1. You are ultimately investing to generate cash flow; cash flow needed either today or in the future.

2. Cash flow has an extremely important hurdle to overcome: the loss of purchasing power. You might otherwise know this as inflation.

Our approach to building a portfolio focused on dividend growth is to invest in “Every”-type companies: Everyone, everywhere, everyday buys their products and services.

Think about the companies you buy household essentials from: your toothpaste, medicines, cleaning products, snacks and beverages. Consider companies whose stores you visit when you are working on a house project or routine home maintenance. And don’t forget the companies that deliver the packages after your online ordering spree.

These companies often have strong financials with growing profits. Though dividend are not guaranteed and can be reduced or eliminated, we seek to include companies with a demonstrated history of consistent payments through good times and bad. They have a competitive advantage and an established global presence offering products to consumers and businesses around the world.

Investment success is measured based on income generated from the investment, not just the value of the investment. We seek to provide consistent income that grows at a rate exceeding inflation through the benefits offered by recurring dividends paid by these types of companies. Investors who only spend the income from their investments may not worry about a temporary loss in value. If that income is not necessary today, it can be reinvested, adding to portfolio for future income needs.

A Differentiated Approach

Investors today face a common misconception about how to define risk in relation to their financial life and their investment portfolios. Many advisers, money managers and media pundits tell investors the primary risk to their life savings is volatility – or how much the portfolio swings in value.

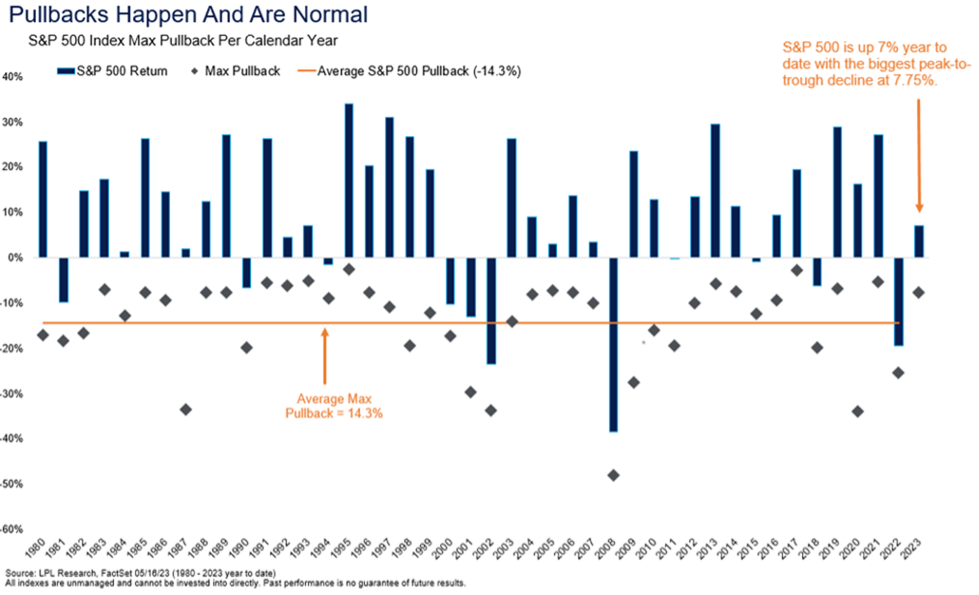

Fluctuations in the value of portfolios and markets are a feature of investing, rather than an abnormal risk. In an average year since 1980, stocks have fallen 14% intra-year and ended the year 10% higher. Additionally, stocks experience an average of three 5-10% pullbacks and one 10% or larger correction each year.

When defining volatility as risk, the focus becomes making sure the value continues to grow enough that it supports the withdrawals an investor needs to make to meet their spending needs. Focusing too much on the value of the portfolio ignores the most significant risk investors face: failing to generate an income stream that keeps up with, if not outpaces your cost of living.

It’s no secret that over your lifetime the things that you buy get more expensive. The risk is not that the value of the portfolio is swinging, rather, the risk is that your income does not grow at the same rate or a higher rate than inflation – meaning you can’t maintain the same lifestyle as you had 10, 20, 30 years ago.

You don’t take the value of your portfolio to restaurants and the grocery store to pay for food. You take the cash income generated from your portfolio.

Advisors typically invest client funds into a basket of mutual funds, which introduces additional fees, as well as additional tax implications for non-qualified accounts. Investing directly in companies helps to minimize those extraneous fees and affords more control over the structure of your portfolio, allowing us to focus your investments on companies that pay and are likely to grow their dividends in the future.

An Example

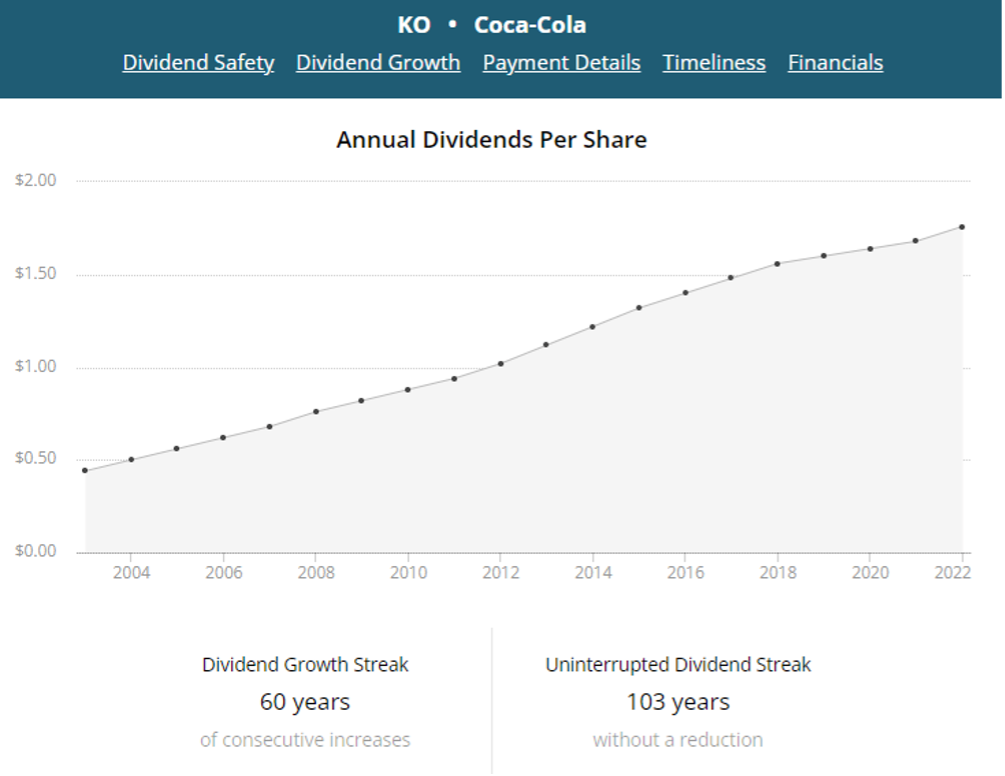

Take an example directly from the portfolio of Warren Buffett.

Buffett noted the power of dividend growth in the latest annual report for his company Berkshire Hathaway when he stated:

“The cash dividend we received from Coke in 1994 was $75 million. By 2022, the dividend had increased to $704 million. Growth occurred every year, just as certain as birthdays. All Charlie and I were required to do was cash Coke’s quarterly dividend checks. We expect that those checks are highly likely to grow.”

We might not all be fortunate enough to collect a $700 million dividend check. But by owning a diversified portfolio of quality companies that are likely to pay and grow dividends, we can align our hard-earned life savings with an investment strategy that attempts to meet our future income needs.

A Lifetime of Evidence

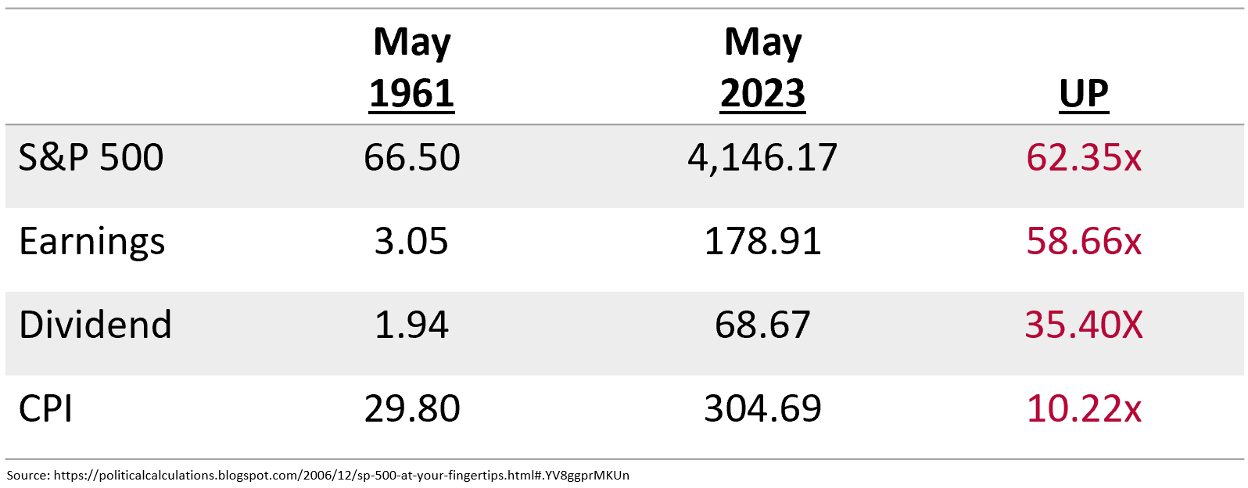

According to the 2023 Retirement Confidence Survey, the median retirement age in America is 62 meaning the average retiree was born in 1961.

In May 1961, the S&P500 index was roughly 66.50. The companies comprising the index generated $3.05 in earnings per share and paid $1.94 in dividends. The Consumer Price Index (CPI) was 29.80.

In the 60 years since, those retirees would see the CPI increase to 304.69. In other words, life got 10x more expensive.

During that same period, the earnings generated by the companies in the S&P500 increased to $178.91 – a 58x increase.

The dividends paid to shareholders by those companies increased to $68.67 – a 35x increase.

The lesson is simple: The cash flow paid to investors increased over three times more than the cost of living.

All the while, the value of S&P500 index rose from 66.50 to 4146.17 – a 62x increase.

Investing in companies that grow their earnings and dividends paid to shareholders allows investors to potentially generate income from their investment portfolio that has historically grown at a faster rate than inflation.

If you are interested in learning more about how this strategy might work in your portfolio, please reach out to schedule a conversation.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual

All performance referenced is historical and is no guarantee of future results

All indices are unmanaged and may not be invested into directly.

Investing involves risk, including possible loss of principal.

Dividend payments are not guaranteed and may be reduced or eliminated at any time by the company.